The 2026 Affordable Care Act (ACA) Open Enrollment results reflect a market that is evolving rather than contracting. While headline figures point to a modest decline in total enrollment, the broader data signals stabilization following several years of rapid growth. At the same time, shifts in plan selection and eligibility are increasing consumer exposure to out-of-pocket costs, reinforcing the need for more intentional coverage strategies.

For advisors, the implications are clear. As consumers gravitate toward lower premiums and higher deductibles, the role of plan selection alone becomes less sufficient. The opportunity now lies in structuring coverage in a way that addresses both financial risk and tax efficiency.

One of the most significant developments in 2026 is the expansion of health savings account (HSA) eligibility. Approximately 43% of enrollees are now in HSA-qualified plans1, largely due to legislative changes that extended eligibility to all Bronze and Catastrophic plans. Despite this expansion, most consumers are not actively selecting plans based on HSA compatibility. Instead, they are choosing lower-premium options and becoming eligible by default, often without understanding or utilizing the associated tax advantages.

This gap presents a clear opportunity for advisors. Establishing an HSA early remains critical, as only expenses incurred after the account is opened qualify for tax-advantaged treatment. Even minimally funded accounts preserve eligibility, while delayed setup can result in the permanent loss of tax benefits on early medical expenses. In practice, this makes timing more important than contribution level, a distinction that is frequently overlooked.

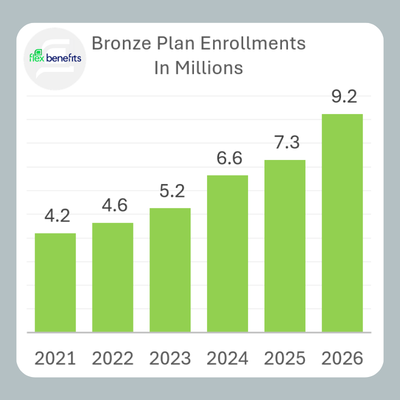

At the same time, plan selection trends indicate a continued shift toward lower-premium, higher-deductible coverage. Bronze plan enrollment has grown to 40% of total enrollments1, while the share of Silver plan selections has declined sharply, reducing reliance on cost-sharing reduction designs. As a result, more consumers are assuming greater financial responsibility at the point of care, often facing deductibles and out-of-pocket maximums that can exceed $10,000.

This environment underscores the value of pairing first-dollar supplemental benefits with HSA-qualified plans. First-dollar products such as accident, critical illness, and hospital indemnity coverage provide immediate cash payments upon a qualifying event, helping offset expenses before the deductible is met. These benefits address short-term liquidity concerns and reduce the likelihood that consumers will defer care or rely on savings and credit to manage unexpected costs.

When combined with an HSA, the result is a more balanced financial strategy. Supplemental benefits provide immediate support at the time of claim, while the HSA offers long-term tax advantages through pre-tax contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Together, they create a structure that addresses both immediate cash flow needs and longer-term financial efficiency, allowing each component to serve a distinct and complementary role.

The 2026 enrollment data1 also shows a modest decline in total ACA participation, with 23.1 million consumers selecting or being automatically re-enrolled in coverage, a decrease of about 1.2 million from the prior year. ICHRA enrollments add new life to the risk pool, while regulators pulled 1.5 million from the market – as unsubstantiated accounts. The overall reduction follows a period of substantial growth and still represents enrollment levels well above those seen in earlier years. In that context, the change is better understood as a normalization of the market rather than a reversal of demand.

For advisors, the implications are clear. As consumers gravitate toward lower premiums and higher deductibles, the role of plan selection alone becomes less sufficient. The opportunity now lies in structuring coverage in a way that addresses both financial risk and tax efficiency. Pairing first-dollar benefits with HSA strategies offers a practical and scalable approach to achieving that objective, while positioning advisors to deliver more comprehensive and differentiated value.

1. Sources: CMS Health Insurance Exchanges 2026 open enrollment report